For many, recent volatility in the stock market has been scary. For young physicians and other potential long-term investors, it can be an opportunity.

Mortgage rates are at their highest level in over a decade. The stock market just hit its lowest point so far in 2022. The Federal Reserve raised the prime rate yet again this year. For many young physicians, this is the first time living through a protracted bear market. Watching your hard-earned savings decrease is viscerally painful. It feels like you are losing everything.

For investors with a long-term horizon, i.e., you don’t need these funds for decades, investing in stocks will ultimately increase your wealth. If you are within a few years of retirement or need to pay college tuition for your kids, that’s a much different scenario.

Let’s back up for a minute…

I’m going to take you way back to January 1, 2000. Pretend you are a brand-new attending and beginning to invest, pay off your debt (interest rates on student loans were much lower then!), and save for a mortgage.

What if I told you there would be a terrorist attack on US soil, the Dot.com boom would crash spectacularly, and a severe subprime mortgage crisis that led the economy into the worst recession since the Great Depression? Oh, and let’s not forget a worldwide pandemic that killed millions of people and shut down the entire globe for months, snarling the economy for years.

How are you feeling right now? Are you excited to invest and save for retirement? Are you jumping up and down to buy your first home? If you’re honest, you are probably concerned and hesitant to invest in anything risky. What if I told you the stock market has been up over 400% since 2000? How is that possible?

First of all, the stock market is not the economy. The stock market is a prediction machine; it looks at the future value of the businesses you invest in. However, none of the events that had the most significant impact on the stock market could be predicted.

But what does that mean for you?

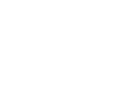

“You might be thinking, what kind of insane pep talk is this?” The point here is that the world breaks every 7-10 years. I can’t tell you what will happen, nor can I tell you when it will happen. But without fail, the most significant events responsible for creating history are the ones we can’t predict.

What can you do to move forward in an economy like this? A bear market is a gift for a young physician just starting their investing life. How can that be? This is an opportunity to buy the same businesses you bought one year ago – Tesla, Apple, Google – at a steep discount. Short-term volatility is the price we pay for long-term growth in the market.

How many of you are dollar-cost averaging your investments over a year? I bet almost all of you do this to some degree. What do I mean by dollar-cost averaging? Most of us buy a chunk of mutual funds and stocks when paid every two weeks or once a month.

Some months the market is up; other months, the market will be down. While there are different arguments when investing a large lump sum, for most of us, that’s simply not how we invest. As working physicians, almost every one of us dollar cost averages throughout our investing lives in our retirement accounts.

Dollar-cost averaging is a forcing function. We buy no matter what. If the market is up, we buy and get a little less for our dollars. When the market is down, guess what, we keep on buying. Except now, we get more value for our dollars.

Think big picture

But Dr. Soelberg, the market is way down this year? The money I invested in 2020 and 2021 has lost 20% or more of its value. I’m ready to sell and sit on cash or bonds.

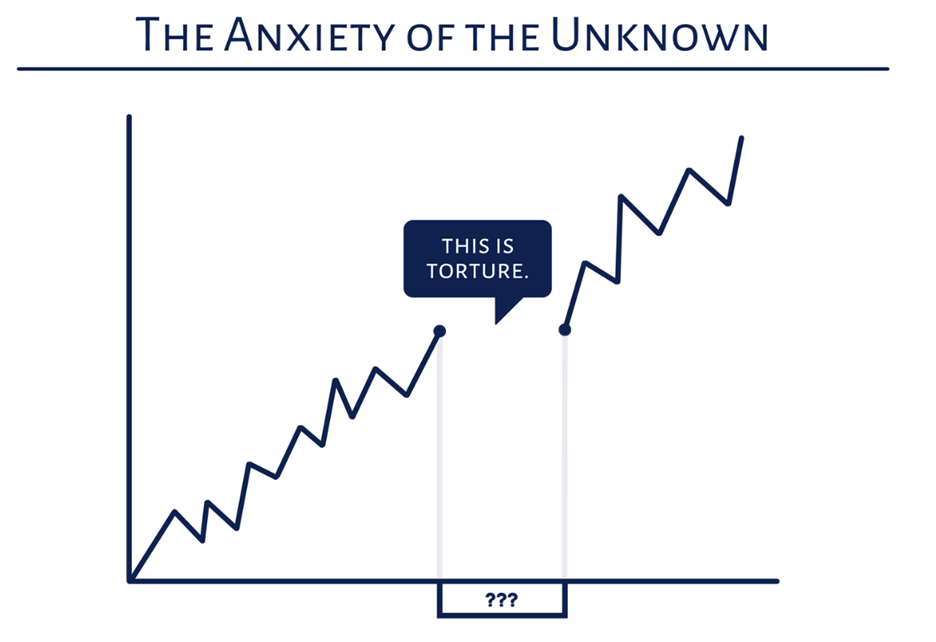

You are correct – this IS a challenging time to invest. Every asset class has been considerably lower since the beginning of 2022– stocks are down 20%, bonds are down 5-10%, and even Bitcoin is 50-70% off its high. While these headwinds seem terrifying, sitting on cash is not the panacea you are seeking.

The late 60s through the early 80s was one of the worst periods to be an investor. The stock market was flat, bonds were flat, and inflation was raging (sound familiar?). And yet, the stock market at least kept up with inflation despite being one of the worst periods ever to invest.

And while it feels safe to invest in cash or bonds, understand that cash lost almost 60% of its value to inflation. Bonds kept up with inflation while being much less volatile than stocks; this is one of the few periods where this is true.

I’ll give you the advice I give my private planning clients, “just keep buying.” We are saving and investing for our future. Nothing provides the returns that stocks will over the long term. Stay the course!

Please share this article if you know any young anesthesiologist that would enjoy or benefit.

This article was originally posted on the American Society of Anesthesiologists Community here.